I’m a loyalty nerd. I received this email from Afterpay with the subject line ‘You’re eligible for an upgrade’, and it had me clicking before I’d finished reading it.

It was a subscription program.

Afterpay Plus, $9.99/month, gives me a virtual Mastercard so I can use pay-in-4 at merchants that don’t natively accept Afterpay. My immediate reaction was…why would I pay for that?

I tried to find out what I was missing…

What you’re actually paying for

Afterpay’s base product is free. You shop at participating merchants, split your purchase into four fortnightly payments, and pay no interest if you stay on track with repayments.

Afterpay Plus charges $9.99/month to do the same thing at merchants that don’t accept Afterpay. Wait, you’re paying a fee to access a financing mechanic that exists precisely because people can’t afford something upfront?

That’s it. That’s the whole product.

The value problem

You’re paying $120/year to access a financing mechanic that, by design, appeals most to people who are cash-flow constrained. There are no rewards, no cashback, no purchase protection. Just payment splitting in more places.

For the maths to work, you’d need to be splitting large, regular purchases at non-Afterpay merchants constantly, and actually deriving real cash flow benefit from it. For most people, it’s just $120 in fees to take on more fragmented debt.

I read on further to find some kind of value proposition.

The messaging problem

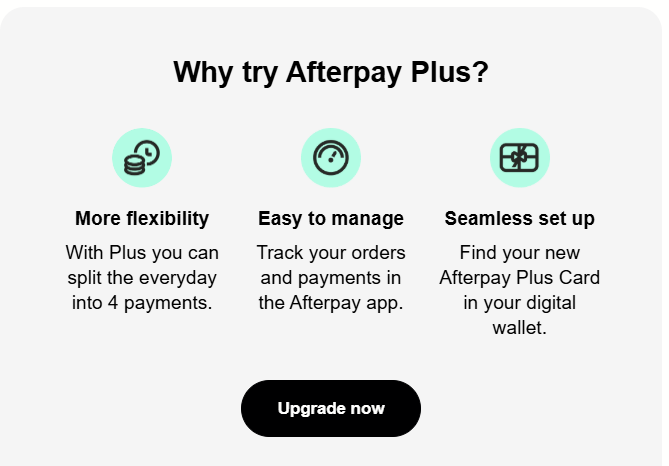

The email offered three reasons to upgrade:

“More flexibility” describes what the product does, not why it’s worth paying for. “Easy to manage” is a feature existing Afterpay users already have, for free. “Seamless set up” is friction reassurance dressed up as a benefit.

Literally zero of the three answer “why is $9.99/month worth it?” There’s no:

- use case framing (“ideal if you regularly shop at X, Y, Z”)

- value anchoring (“split a $400 dentist bill into 4 payments”)

- ROI framing of any kind

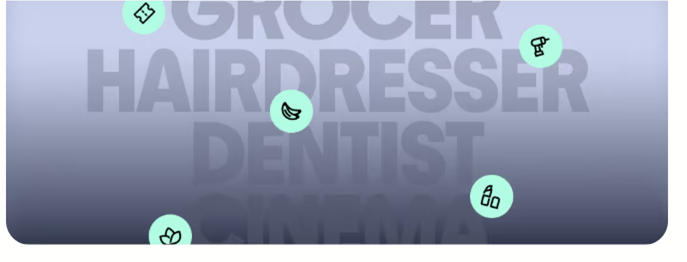

The closest the email gets to a real use case is a decorative visual at the bottom with the words “Grocer, Hairdresser, Dentist, Cinema” floating in a gradient. No copy. No context. The strongest creative idea in the email and it’s completely unsupported.

A competent subscription pitch quantifies value and helps readers self-select. Something as simple as “If you regularly spend at merchants that don’t accept Afterpay, you can split those bills and hold onto your cash for longer” would be a start. That’s still a debatable proposition, but at least it’s a proposition.

The loyalty angle

Afterpay built its entire business on one powerful behavioural mechanic. Remove the friction of upfront payment, and people buy more, more often, at higher average order values. That stickiness is real. Customers who use Afterpay regularly are embedded in it.

Afterpay Plus is an attempt to monetise that stickiness through a subscription model. In theory, smart. Subscription loyalty works when the fee creates a commitment device that deepens engagement over time. Amazon Prime is the textbook example where paying the fee creates psychological pressure to extract value, which drives purchase frequency, which deepens the relationship.

Afterpay Plus doesn’t do that. It extends the use case. A wider net, but no loop. There’s no mechanism that makes a Plus subscriber more engaged, more valuable, or more emotionally connected to Afterpay over time. It’s a revenue play dressed as a loyalty play, and the messaging makes that obvious because nothing in the email speaks to who the customer is or why they should care about the brand beyond the transaction.

Afterpay has been here before

This isn’t Afterpay’s first swing and miss. I wrote about Afterpay’s formal loyalty program before it was quietly pulled, and the same structural issues were present then. A product that didn’t clearly articulate why customers should care, with messaging that listed features instead of making an argument.

You can read that piece here: Afterpay’s loyalty program is an afterthought

The pattern is consistent. Afterpay has genuine, earned engagement at the transactional level. What it hasn’t figured out is how to translate that into a loyalty or subscription proposition customers actually want to pay for.

The bottom line

This is a paid layer on top of a free product with a thin use case, and the messaging doesn’t even attempt to make the economics compelling. The email reads like it was written to announce the feature internally and accidentally sent to customers.

Afterpay Plus might make sense for a very specific consumer with high, regular spend at non-Afterpay merchants who genuinely benefits from smoothing those payments. But the email they sent wouldn’t help that person identify themselves.

It tells you that you’re eligible. It doesn’t give you a reason to want it.

In subscription and loyalty strategy, that’s a very hard position to recover from. Once a customer does the mental arithmetic and lands on “not worth it,” you rarely get a second chance.

Afterpay had my attention. They just didn’t have an argument.