The loyalty industry has developed a comfortable habit of explaining consumer behaviour through a generational engagement lens. Gen Z want instant rewards. Boomers stay loyal to a handful of trusted brands. Millennials want experiences. Gen X are the engagement sweet spot. These observations are real, measurable, and consistently supported by research. But they are descriptions, not explanations.

At Loyalty & Reward Co, we argue that the primary driver underlying most demographic differences in loyalty program behaviour is not generational identity per se. It is disposable income. Get that variable right and much of the observed variation across age groups starts to make sense in a way that has genuine implications for how programs should be designed.

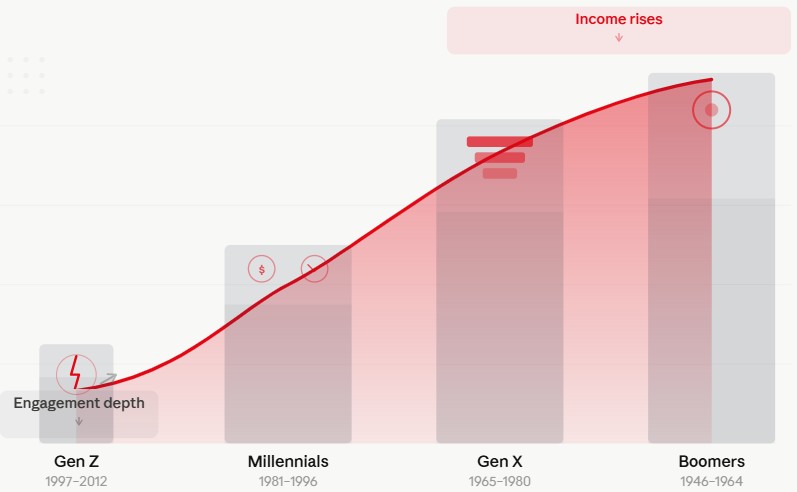

What the data actually shows

The evidence on generational differences is broadly consistent across major studies. According to research compiled across sources including Bond Brand Loyalty, EY, Deloitte, and ITA Group, membership rates and program depth follow a clear arc by generation.

Baby Boomers (born 1946-1964) hold memberships in one to three programs on average, with 50-60% participating in at least one. They favour simple structures, quality-based rewards, traditional communication channels, and brand familiarity. Only 26% prefer cashback rewards, the lowest of any generation. Once established in a program, they are among the least likely to switch.

Gen X (born 1965-1980) are the power users. With 60-75% holding memberships and an average of three to five programs per consumer, they are simultaneously the broadest engagers and among the most pragmatic. They prize data security, respond well to tiered structures, and are overtly status-driven. Fuel discounts, grocery coupons, and frequent-flyer miles keep them active. Eighty-seven percent view data protection as critical (Mando-Connect, 2023/2024).

Millennials or Gen Y (born 1981-1996) show membership rates broadly similar to Gen X at 60-70%, but with a distinct dual orientation: they are financial realists and experience seekers simultaneously. They record the highest cashback preference of any generation at 41% (PYMNTS, 2024), yet also crave VIP treatment, early access, and members-only events. The Economic recessions that shaped their early careers explain the financial pragmatism; their formative relationship with digital platforms explains the appetite for personalisation and social integration.

Gen Z (born 1997-2012) present the most distinctive profile, with lower membership rates of 40-50%, smaller program portfolios of two to three on average, a strong preference for instant rewards, and high programme churn: 43% will switch to a better-fitting program quickly (Forbes Business Council, 2023). Ninety-four percent are eager to earn rewards, but 41% are dissatisfied with current offerings. They want mobile-first, values-aligned, immediately gratifying programs. And 73% say they are willing to pay more for sustainable products (McCrindle, 2025).

Income as the organising principle

The standard industry explanation treats these differences as products of generational psychology, digital nativity, or shifting cultural values. All of these factors play a role. But they obscure something more fundamental.

Consider the behaviour most associated with Gen Z: a preference for instant cashback over long-term points accumulation. The behavioural economics framing, specifically hyperbolic discounting (Frederick, Loewenstein & O’Donoghue, 2002), describes this as present bias: the tendency to weight immediate rewards more heavily than future ones, even when the future reward is objectively larger. This construct is often applied as if it were a generational trait. It is not. It is a universal human tendency that intensifies under financial constraint.

When you are managing tight margins between income and rent, choosing not to lock your discretionary spending into a points program for a flight redemption that is two years away is not impulsive. It is rational. Instant cashback that offsets grocery costs next week is simply worth more when your time horizon is compressed by necessity.

The corollary of this is also instructive. Gen X, with established careers, homeownership, and growing discretionary income, can afford to play a longer game. The investment required to achieve Qantas Platinum or Marriott Bonvoy Titanium status, measured in both spending and cognitive attention, is accessible to consumers who have the financial and temporal flexibility to make it. Their heavy multi-program engagement, status orientation, and willingness to modify behaviour to protect accumulated benefits (McCaughey & Behrens, 2011, found FFP members accept up to a 6% price premium to avoid losing accumulated benefits) reflects the engagement patterns of people with enough slack in their finances to treat loyalty as an investment.

Baby Boomers present an interesting counterpoint. They have among the highest disposable incomes of any cohort, often with reduced mortgages, grown children, and superannuation assets generating income. Yet they engage with fewer programs and prefer simpler structures. This is where life stage modifies the income relationship. Financial complexity becomes less appealing, not because Boomers cannot manage it, but because they no longer need to. They have less to prove, established brand relationships that have earned trust over decades, and less appetite for the gamified complexity younger generations have been socialised into. Simplicity is a choice, not a constraint.

The Millennial profile sits at the intersection of income recovery and elevated expectations. Shaped by the 2008 financial crisis, many entered their highest earning years later than previous generations and carried student debt that suppressed disposable income through their twenties. The 41% cashback preference reflects residual financial pragmatism. The parallel appetite for VIP experiences and experiential rewards reflects aspirational consumption patterns as their financial position improves. The Bond Brand Loyalty Loyalty Report (2023) consistently found Millennials among the most program-engaged cohorts in absolute terms once income stabilises.

What psychology tells us about the mechanisms

The income hypothesis is strengthened when examined through established psychological constructs.

Loss aversion (Kahneman & Tversky, 1979) predicts that the pain of losing something is approximately twice as powerful as the pleasure of gaining the same thing. This creates powerful retention dynamics in tiered programs: the threat of losing Gold or Platinum status drives behaviour modifications that defied rational cost-benefit analysis. But loss aversion requires something to lose in the first place. A Gen Z member who has never invested in achieving status has no accumulated benefit to protect. Loss aversion as a loyalty mechanism is effectively only available to consumers who have had the financial bandwidth to accumulate in the first place.

Social identity theory (Tajfel & Turner, 1978) explains why tier status generates loyalty outcomes that transcend the material benefits. Research by Drèze & Nunes (2009) demonstrated that elite tier labels drive status perceptions and in-group/out-group dynamics independent of actual reward values. Ivanic (2015) found that high-status tier members engage in status-reinforcing behaviours even when doing so offers no material benefit. The desire for status-based recognition through loyalty programs is consistent across generations, but the ability to earn and maintain it follows income.

Value alignment research provides one area where the generational explanation holds more strongly on its own terms. Liu-Thompkins & Taheran (2023), in a multi-country study across the US, UK, Australia, and India (N > 4,000), found that 77% of under-35 consumers consider value alignment important in loyalty decisions, compared to approximately 38% of those aged 65+. The 18-24 age group is uniquely oriented toward positive brand affiliation: they are more likely to reward alignment (63%) than punish misalignment (51%), the reverse of every other age cohort. This is a genuine generational effect, shaped by cohort-specific values formation and exposure to social media culture, not primarily by income. Gen Z’s 73% willingness to pay more for sustainable products (McCrindle, 2025) reinforces this.

Similarly, the preference for digital-native program experiences, native apps, gamification, TikTok-integrated challenges, and social proof mechanics reflects genuine differences in technology relationship that are not reducible to income. These are cohort effects produced by the digital environment in which Gen Z developed. But even here, the income lens adds nuance: gamification and social engagement are cheap forms of loyalty currency for programs targeting younger consumers who cannot be engaged through aspirational travel rewards.

The trajectory argument

Perhaps the strongest evidence for the income hypothesis is the longitudinal prediction it generates: as cohorts age and their incomes rise, their loyalty program behaviour should converge toward the engagement patterns of higher-income older cohorts.

There is reasonable support for this in the data. Millennials, who showed cashback-dominant preferences and lower tiered program engagement in their twenties, have moved toward the multi-program, status-oriented patterns of Gen X as their earnings have grown. The Deloitte (2024) and EY (2025) surveys both note increased Millennial interest in premium and tiered programs as that cohort moves through peak earning years.

If this trajectory holds for Gen Z, then many of the loyalty strategies currently being developed to serve their preference for instant gratification and mobile-first simplicity are, at best, appropriate for now and likely to require significant recalibration in a decade. This does not mean those strategies are wrong. Meeting members where they are is always the right starting point. But programs designed purely around Gen Z’s current preferences may underestimate the future engagement capacity of that cohort as their financial circumstances change.

What this means for program design

The income hypothesis is not an argument against demographic segmentation. The differences between generations are real, measurable, and actionable. But it does have specific implications for how designers should use those differences.

Design for the member’s current life stage, not just their birth year. A 26-year-old with a graduate income and no dependants has meaningfully different loyalty behaviour potential than a 26-year-old managing debt and rent pressure. Age is a proxy; disposable income and discretionary spending flexibility are the underlying variables.

Build programs with accessible entry points and scalable depth. The most durable program architectures offer immediate, tangible value at entry (meeting Gen Z and constrained Millennials where they are) while creating clear pathways toward deeper engagement, status accumulation, and aspirational redemption as member income grows. This is not just good generational design; it is good lifecycle design.

Do not write off younger members as low-engagement. The goal gradient effect (Kivetz, Urminsky & Zheng, 2006) demonstrates that visible progress toward a valued goal accelerates engagement. Younger members who are shown a clear, credible path to genuinely valuable aspirational rewards, and who experience meaningful progress toward them, can exhibit the same acceleration patterns as any other cohort. The design challenge is making those paths feel attainable given current financial constraints.

Respect the non-negotiables that are genuinely generational. Mobile-first is not a preference for Gen Z, it is a baseline expectation. Values-based programming is not niche, it is increasingly mainstream across all cohorts but especially under-35s. Data privacy is not just a Gen X concern: 87% of Gen X rate it critical (Mando-Connect, 2023/2024), but younger consumers are increasingly attentive to data practices as awareness grows (Forbes Business Council, 2024; Balabanis et al., 2025). These are real generational effects that income does not fully explain.

The bottom line

Generational differences in loyalty program engagement are real and well-documented. Baby Boomers value simplicity and trust. Gen X are power users who engage broadly and status-driven. Millennials balance financial pragmatism with experiential aspiration. Gen Z want immediacy, authenticity, and mobile convenience.

But the most plausible explanation for much of this variation is not generational character. It is access to discretionary income, and the financial confidence to treat loyalty as a long-term investment rather than a short-term transaction. Programs that understand this can design not just for who a member is today, but for who they will become as their financial lives develop.

That is the design opportunity the industry has largely not yet claimed.

Industry and practitioner sources

Balabanis, G. et al. (2025). ‘Cultural Influences on Privacy Calculus in Loyalty Programs.’ https://www.tandfonline.com

Bond Brand Loyalty (2023). The Loyalty Report 2023. https://info.bondbrandloyalty.com/loyaltyreport-2023-2-0

Boston Consulting Group (2024). ‘Loyalty programs customer expectations growing.’ https://www.bcg.com/capabilities/marketing-sales/customer-loyalty-programs

Deloitte (2024). ‘New generation of consumers brings new expectations around loyalty.’ https://action.deloitte.com/insight/4083/new-generation-of-consumers-brings-new-expectations-around-loyalty

EY (2025). 2025 EY Loyalty Market Survey Report. https://www.ey.com/en_us/cmo/ey-loyalty-market-study

Forbes Business Council (2023). ‘Cracking the code of Gen Z loyalty programs.’ https://www.forbes.com/councils/forbesbusinesscouncil/2023/03/14/cracking-the-code-of-gen-z-loyalty-programs

Forbes Business Council (2024). ‘Loyalty programs and data collection: Navigating the privacy-first era.’ https://www.forbes.com/councils/forbesbusinesscouncil/2024

Hure, D. (2025). ‘What do digital natives really want from loyalty programs?’ https://www.linkedin.com/pulse/what-do-digital-natives-really-want-from-loyalty-programs-denis-hure

ITA Group (2025). ‘What do customers want from loyalty programs?’ https://www.itagroup.com/insights/loyalty/what-customers-want-loyalty-programs

Johnson, Z. (2024). ‘How retail banks can win over Gen Z: Tailoring credit rewards for a digital-first generation.’ https://www.linkedin.com/pulse/how-retail-banks-can-win-over-gen-z-zachary-johnson

KPMG (2024). ‘Unconditional love: How to make customers faithful with loyalty.’ https://assets.kpmg.com/content/dam/kpmg/sg/pdf/2024/02/unconditional-love-how-to-make-customers-faithful-with-loyalty.pdf

Mando-Connect (2023, updated 2024). Understanding Loyalty in Europe. https://mando.co.uk/understanding-loyalty-in-europe/

McCrindle (2025). ‘Generational consumer profiles.’ https://mccrindle.com.au/article/topic/generation-z/gen-z-consumer-profile

McKinsey & Company (2023). ‘Mind the gap: Curated reads for Gen Z — and their Z-curious colleagues.’ https://www.mckinsey.com/featured-insights/mckinsey-explainers/what-is-gen-z

Mika, A. (2025). ‘Generational differences in brand loyalty.’ https://www.linkedin.com/pulse/generational-differences-brand-loyalty-alex-mika

Oracle (2020). ‘How to engage customers across every generation.’ https://www.oracle.com/cx/loyalty/customer-loyalty-generations

Pérez, M. (2025). ‘How gamified experiences are winning over Gen Z consumers.’ https://www.forbes.com/councils/forbesbusinesscouncil/2025

PYMNTS (2024). ‘Boomers prefer email, Gen Z’s opt for apps as top choice for reward delivery.’ https://www.pymnts.com/consumer-insights/2024/boomers-prefer-email-gen-zs-opt-for-apps-as-top-choice-for-reward-delivery

PYMNTS (2024). ‘More than 30% of card users opt for cash back rewards.’ https://www.pymnts.com/consumer-finance/2024/more-than-30-of-card-users-opt-for-cash-back-rewards

Statista (2024). ‘Loyalty program influence by generation: UK.’ https://www.statista.com/topics/loyalty-programs-united-kingdom

TTG (2024). ‘How each generation values privacy: Strategies for marketers.’ https://www.ttgmedia.com/news/how-each-generation-values-privacy-strategies-for-marketers

Academic sources

Drèze, X. & Nunes, J.C. (2009). Feeling superior: The impact of loyalty program structure on consumers’ perceptions of status. Journal of Consumer Research, 35(6), pp890-905. https://doi.org/10.1086/593946

Frederick, S., Loewenstein, G. & O’Donoghue, T. (2002). Time discounting and time preference: A critical review. Journal of Economic Literature, 40(2), pp351-401. https://doi.org/10.1257/002205102320161311

Ivanic, A.S. (2015). Status has its privileges: The psychological benefit of status-reinforcing behaviors. Psychology & Marketing, 32(7), pp697-708. https://doi.org/10.1002/mar.20813

Kahneman, D. & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), pp263-291. https://doi.org/10.2307/1914185

Kivetz, R., Urminsky, O. & Zheng, Y. (2006). The goal-gradient hypothesis resurrected: Purchase acceleration, illusionary goal progress, and customer retention. Journal of Marketing Research, 43(1), pp39-58. https://doi.org/10.1509/jmkr.43.1.39

Liu-Thompkins, Y. & Taheran, S. (2023). The Future of Loyalty Report. Loyalty Science Lab, Strome College of Business, Old Dominion University. https://loyaltysciencelab.com

McCaughey, N. & Behrens, A. (2011). Flying for fun or profit: Frequent flyer loyalty programs and the passenger’s willingness to pay. Journal of Transport Economics and Policy, 45(2), pp293-311. https://www.jstor.org/stable/23072075

Melnyk, V. & Bijmolt, T. (2015). The effects of introducing and terminating loyalty programs. European Journal of Marketing, 49(3/4), pp398-419. https://doi.org/10.1108/EJM-12-2013-0694

Tajfel, H. & Turner, J.C. (1978). An integrative theory of intergroup conflict. In W.G. Austin & S. Worchel (Eds.), The Social Psychology of Intergroup Relations (pp33-47). Brooks/Cole. https://psycnet.apa.org/record/1979-07066-000